TL;DR

If you are an NRI Residential or returning Indian, your tax liability in India depends entirely on your residential status under Section 6 of The Income Tax Act.

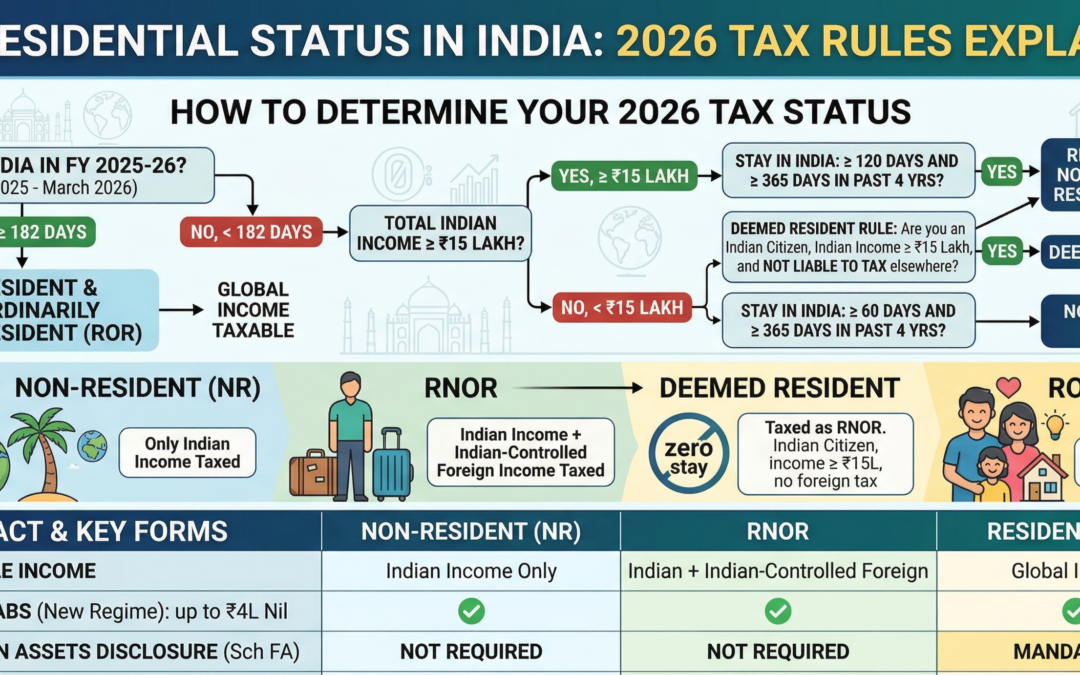

Key rules include:

- Stay ≥182 days in India → Resident

- Stay ≥120 days with income > ₹15 lakh → possible RNOR

- Stay <120 days → usually Non-Resident

- Residents pay tax on global income

- NRIs pay tax only on Indian income

Understanding these rules helps avoid accidental tax residency and unexpected taxation on foreign income.

Why Residential Status Matters for NRIs

Many NRIs assume that their passport, visa, or NRI bank account determines tax status.

That is incorrect.

In India, tax residency depends solely on physical presence and income thresholds.

The Income Tax Department determines your status each year using Section 6 of the Income Tax Act.

Your residential status decides:

- Whether global income becomes taxable

- Reporting obligations for foreign assets

- Eligibility for NRE/NRO account benefits

- Applicability of DTAA relief

Residential Status Under Section 6 of the Income Tax Act

| Residential Status | Meaning |

|---|---|

| Resident and Ordinarily Resident (ROR) | Global income taxable in India |

| Resident but Not Ordinarily Resident (RNOR) | Limited taxation |

| Non-Resident (NRI) | Only Indian income taxable |

The 182-Day Rule Explained

The basic residency rule states:

An individual becomes resident in India if they stay in India for 182 days or more in a financial year.

Example

An NRI working in Dubai spends:

- April–June: 60 days

- September: 40 days

- December–February: 90 days

Total stay = 190 days

Result:

- Residential Status → Resident in India

- This may trigger global taxation of income.

- The 120-Day Rule for High-Income NRIs

Since the Finance Act 2020, additional rules apply to NRIs.

If:

- Indian income exceeds ₹15 lakh, and

Stay in India 120 days or more but less than 182 days - The person may become Resident but Not Ordinarily Resident (RNOR).

- This rule prevents high-income NRIs from maintaining NRI status while spending significant time in India.

Types of Residential Status in India

1. Non-Resident (NRI)

An individual is Non-Resident if they do not satisfy the residency conditions.

- Tax Impact

- Only Indian-sourced income taxed

- Foreign income not taxable

Example taxable income:

- Rent from Indian property

- Interest from NRO accounts

- Capital gains from Indian shares

2. Resident but Not Ordinarily Resident (RNOR)

RNOR is a transitional tax status, typically applicable to:

- Returning NRIs

- Individuals spending more time in India

RNOR applies if:

- Resident in India but

- Not resident for 2 out of last 10 years OR

- Stayed less than 730 days in last 7 years

- Tax Benefit

RNOR individuals:

- Pay tax on Indian income

- Foreign income generally not taxable

This creates a tax planning window of 2–3 years.

3. Resident and Ordinarily Resident (ROR)

You become ROR if you satisfy both:

- Resident in 2 of last 10 years

- Stayed 730 days in last 7 years

- Tax Impact

All global income becomes taxable in India:

- Foreign salary

- Overseas investments

- Offshore rental income

- Foreign dividends

RNOR Status: A Powerful Tax Planning Window

For returning NRIs, RNOR status can be extremely valuable.

During RNOR years you can:

- Reorganize foreign investments

- Transfer overseas assets

- Liquidate foreign portfolios

- Plan tax-efficient repatriation

Many professionals miss this opportunity and become fully taxable earlier than necessary.

Tax Implications Based on Residential Status

| Income Type | NRI | RNOR | ROR |

|---|---|---|---|

| Indian salary | Taxable | Taxable | Taxable |

| Indian rental income | Taxable | Taxable | Taxable |

| Foreign salary | Not taxable | Usually not taxable | Taxable |

| Foreign investments | Not taxable | Not taxable | Taxable |

| Foreign capital gains | Not taxable | Not taxable | Taxable |

Step-by-Step: How to Determine Your Residential Status

Step 1

- Calculate total days spent in India in the financial year

Step 2

- Check if stay ≥182 days

If yes → Resident

Step 3

- Check 120-day rule

Applicable if:

Indian income > ₹15 lakh

Step 4

- Apply RNOR conditions

Evaluate:

- Residence in last 10 years

- Stay in last 7 years

- Common Mistakes NRIs Make

1. Tracking calendar year instead of financial year

India counts April–March.

2. Ignoring travel history

Residential status may require 4-year lookback.

3. Accidental residency

Long family visits often trigger 120-day rule.

4. Not planning RNOR benefits

This may cause unnecessary taxation of foreign income.

Practical Example

Scenario

NRI software engineer in the US:

Indian income: ₹18 lakh

Stay in India: 140 days

Result:

Not NRI

Status = RNOR

Foreign income remains outside Indian tax scope temporarily.

When NRIs Should Seek Professional Tax Advice

Professional tax planning becomes essential if you:

- Are returning to India permanently

- Have foreign investments

- Earn income in multiple countries

- Need DTAA tax relief

- Own property in India

Expert guidance ensures:

- Correct residential status classification

- Optimized tax planning

- Compliance with disclosure requirements

Conclusion

Determining NRI residential status in India is critical for tax planning.

Even a small change in the number of days spent in India can significantly impact taxation of global income.

Key takeaways:

- Monitor 182-day and 120-day rules

- Plan travel carefully

- Use RNOR years strategically

For NRIs and returning professionals, working with experienced tax advisors ensures compliance while minimizing tax exposure.

Need expert guidance on NRI taxation?

Consult the specialists at Sunil K Khanna & Co., Chartered Accountants in Gurgaon & Delhi, for comprehensive NRI tax advisory and compliance support.

6. FAQ SECTION

What is the 182-day rule for NRI?

If an individual stays in India for 182 days or more during a financial year, they become a resident for tax purposes.

What is RNOR status?

RNOR means Resident but Not Ordinarily Resident, a transitional tax status where foreign income is generally not taxed in India.

Do NRIs pay tax on foreign income in India?

No. NRIs are taxed only on income earned or received in India.

What happens if an NRI stays more than 120 days in India?

If Indian income exceeds ₹15 lakh and stay exceeds 120 days, the person may become RNOR.

How many years does RNOR status last?

Typically 2–3 financial years, depending on travel history and previous residence status.

Is residential status checked every year?

Yes. Residential status is calculated separately for every financial year.

BLOG BY : Sunil k khanna & Co.